Economic systems are fundamental to the functioning of any society. They determine how resources—such as labor, land, and capital—are allocated and utilized. The economic system of a country influences everything from the prices of goods and services to the standard of living for its citizens. Understanding economic systems is essential not only for students of economics but also for anyone wishing to comprehend the world’s functioning in terms of resource management, wealth distribution, and decision-making processes.

In this article, we will explore the different types of economic systems, their characteristics, advantages and disadvantages, and how they shape societies and the global economy.

What is an Economic System?

An economic system refers to the organized way in which a country or society manages its resources, production, and distribution of goods and services. It provides a framework for deciding what to produce, how to produce, and for whom to produce, with the goal of meeting the needs and wants of its population.

Economic systems can vary widely based on the level of government control, the role of private ownership, and the degree of market competition. The decisions within these systems shape the economic activities of the country, such as labor, trade, and investment. There are several types of economic systems, each having distinct features and philosophies about how the economy should function.

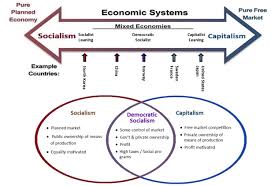

Types of Economic Systems

There are four primary types of economic systems, each with its own approach to managing resources:

- Traditional Economy

In a traditional economy, decisions about production and distribution are made based on customs, traditions, and historical precedent. These systems are often found in rural or agricultural societies where resources are shared within families or small communities. The roles of individuals are generally predetermined by tradition, and economic change tends to occur slowly.

Characteristics of Traditional Economy:

- Production is based on subsistence farming and bartering.

- Technology is often limited, as methods of production are passed down through generations.

- Little emphasis is placed on economic growth or innovation.

- There is a focus on community and family ties rather than individual wealth.

Examples: Indigenous communities in parts of Africa, Asia, and the Arctic.

Advantages:

- Strong social cohesion and community bonds.

- Sustainable practices as economies are based on natural resources.

- Predictability in work roles and economic activities.

Disadvantages:

- Limited access to modern technology and capital.

- Little room for economic growth or diversification.

- Vulnerability to environmental changes and external economic shocks.

- Command Economy (Planned Economy)

A command economy is one in which the government plays a central role in making economic decisions. In this system, the government owns the means of production, such as factories, land, and resources, and directs their use according to a central plan. The aim is often to achieve equality and redistribute wealth in a more controlled manner.

Characteristics of Command Economy:

- The government controls what goods and services are produced, in what quantities, and at what price.

- Limited consumer choice since the government determines the supply of goods.

- Little competition or private ownership.

- The emphasis is on central planning and the equitable distribution of wealth.

Examples: The former Soviet Union, North Korea, and Cuba.

Advantages:

- Can result in rapid industrialization and the achievement of large-scale infrastructure projects.

- The government can focus on reducing inequality and providing basic services to all citizens.

- There is a focus on long-term planning rather than short-term profits.

Disadvantages:

- Lack of consumer choice and innovation, as the government dictates supply.

- Inefficiencies in production and distribution due to the absence of market signals (e.g., prices).

- Possible suppression of individual freedoms and creativity.

- Risk of economic stagnation, as there is little incentive for businesses or individuals to improve.

- Market Economy (Capitalism)

In a market economy, the production and distribution of goods and services are driven by the forces of supply and demand, with minimal government intervention. Businesses and individuals are free to make their own decisions about what to produce, how to produce, and for whom to produce. Profit motives, competition, and consumer preferences determine the flow of resources in the economy.

Characteristics of Market Economy:

- Private ownership of the means of production.

- Competition among firms, which drives innovation and efficiency.

- Prices are determined by market forces, where supply and demand meet.

- Consumer choice is central, and the economy is typically more dynamic and adaptable.

Examples: The United States, most Western European countries, and Japan.

Advantages:

- High levels of innovation and technological advancement due to competition.

- Efficient allocation of resources, as prices reflect consumer demand.

- Greater economic freedom for individuals and businesses.

- A wide range of goods and services available to consumers.

Disadvantages:

- Inequality in wealth distribution, as some people and companies thrive while others may struggle.

- Overemphasis on profit, which can lead to environmental degradation and worker exploitation.

- The potential for market failures, where certain goods or services (like public health or education) are under-provided.

- Economic instability, as fluctuations in the market can lead to recessions or unemployment.

- Mixed Economy

A mixed economy blends elements of both market and command economies. In this system, private and public sectors coexist, with the government playing a role in regulating and correcting market failures while allowing the private sector to operate freely. This system seeks to balance the efficiency of market mechanisms with the need for social welfare and public goods.

Characteristics of Mixed Economy:

- Private ownership of businesses and property, alongside government intervention in certain sectors.

- The government may regulate industries, provide public goods and services (e.g., healthcare and education), and intervene in cases of market failure.

- There is a degree of wealth redistribution through taxes and social welfare programs.

- The economy allows for both market competition and government oversight.

Examples: Most modern economies, such as the United Kingdom, Canada, Australia, and India.

Advantages:

- Combines the efficiency of the market with the goal of addressing social inequalities.

- The government can address issues such as poverty, healthcare, and education, which are underprovided in purely market economies.

- Greater economic stability and protection against extreme economic fluctuations.

Disadvantages:

- Can lead to inefficiency if government intervention is too heavy-handed.

- May face challenges in balancing private profit motives with public good.

- The risk of too much government regulation stifling innovation and competition.

Key Questions About Economic Systems

Understanding the various economic systems also requires addressing some key questions:

- What should be produced?

This refers to the basic problem of deciding what goods and services are needed to meet society’s needs. A traditional economy focuses on what has always been produced, while a market economy responds to consumer demand. - How should goods and services be produced?

The method of production depends on available technology and the labor force in the economy. In a command economy, the government dictates methods, while in a market economy, businesses choose the most cost-effective way to produce goods. - For whom should goods and services be produced?

This question addresses the distribution of goods and services within society. In a market economy, goods are distributed based on purchasing power. In a command economy, goods are often allocated according to a government plan, sometimes equally or based on need. - What role should the government play in the economy?

Different economic systems assign varying degrees of responsibility to the government. A command economy features heavy government control, while a market economy advocates minimal government intervention. A mixed economy seeks a balance between the two.

Conclusion

Economic systems are at the heart of how societies organize their resources and address the fundamental problem of scarcity. Whether through tradition, central planning, market forces, or a combination of these elements, the economic system of a country determines the opportunities and challenges its citizens will face.

Each economic system comes with its strengths and weaknesses, and most countries today operate within mixed economies, seeking to combine the best aspects of different systems while mitigating their disadvantages. Understanding these systems helps individuals better comprehend how the world operates and the impact of various economic decisions on their lives.

As students and citizens, it is crucial to recognize that the economic system influences not only financial outcomes but also broader social, environmental, and political landscapes. By understanding these systems, we can better participate in economic discourse, advocate for reforms, and make informed decisions as consumers, workers, and voters.

Key Takeaways

- Economic systems answer the basic questions of what, how, and for whom to produce.

- The four primary types of economic systems are traditional, command, market, and mixed.

- Each economic system has distinct characteristics, advantages, and disadvantages that affect both individuals and societies.

- Mixed economies combine elements of both market and command systems to balance economic efficiency with social welfare.

Understanding economic systems empowers us to see beyond mere market transactions and appreciate the broader social and political forces shaping our world